Management Figures

Fig 1 - Management Figures Page

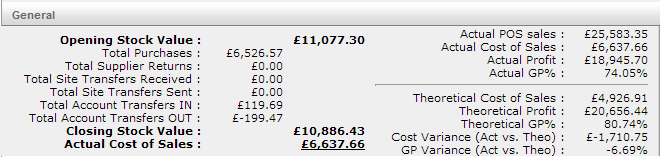

- Opening Stock – Cannot be changed, this is the closing stock from last period. By default it’s the weighted average value.

- Total Purchase – Total value of supplier purchases that have been approved into stock during the period

- Total Supplier Returns – Total value of supplier returns that have been approved out of stock during the period

- Total Site Transfers Received – Total value of site transfers received and approved during the period

- Total Site Transfers Sent – Total value of site transfers issued and approved during the period

- Total Account Transfers In – Total value of account transfers received and approved during the period, this includes things such as petty cash transfers (only appears on the report when affecting COS)

- Total Account Transfers Out – Total value of account transfers issued and approved during the period, such as staff food etc. (only appears on the report when not affecting COS) NB. Best practice advises that Wastage is included in your cost of sales, therefore will not show in this entry however if wastage is not included then this entry will show your wastage included.

- Closing Stock Value – Total value of goods entered in your closing stock by default it’s the weighted average value.

- Actual Cost of Sales – Opening Stock + Purchases- Returns +/- Transfers – Closing Stock

Actual GP

- Actual POS Sales – Total verified Net Sales from Epos i.e. the sales from the till that the system can read using the PLU numbers assigned to that site.

- Actual Cost of Sales – Total cost to run the business during the period (as above)

- Actual Profit – Actual POS Sales – Actual Cost of Sales

- Actual GP – Actual COS/Actual POS expressed as a percentage

Theoretical GP

-

Theoretical Cost of Sales – Quantity sold from total verified PLU’s multiplied by the recipe in the system using the assigned supplier price for the products in the recipe at that site.

- E.g. PLU 123 sold 100 times. PLU 123 = 125ml champagne at Supplier A’s cost price of £1.30 per 125ml. PLU 123 x 100 x £1.30 = cost £130 theoretically.

- Theoretical Profit – Actual POS – Theoretical COS

- Theoretical GP - Theoretical COS/Actual POS expressed as a percentage

- Cost Variance – Theoretical COS – Actual COS

- GP variance – Theoretical GP – Actual GP

Comments

Please sign in to leave a comment.