What’s Changing?

This release note contains all changes made in the system required to allow legislative compliance from April 2021.

Release date: 11th March 2021.

Reason for the Change

Her Majesty’s Revenue and Customs (HMRC) are implementing changes to legislation agreed by the UK government, for the tax year beginning 6th April 2021.

Customers Affected

All customers with the Payroll or Pension module with pay dates on or after 6th April 2021.

Release Notes - Contents

(select a heading from the list below to be taken to that part of the release note)

Payroll Statutory Information Page

PAYE – Tax threshold rates for 2021

Student Loans and Post Graduate Loans

National Minimum Wage (NMW) and National Living Wage (NLW)

Release Notes

Payroll Statutory Information Page

Within the Payroll module, there is a Statutory Information page which contains the rates and allowances for the current and previous tax years. This page is updated annually with the new tax year’s rates.

- To view this page, go to Payroll > Administration > Payroll Statutory Information

Fig.1 – Payroll Statutory Information Page - rates for 2021/22

PAYE – Tax threshold rates for 2021

In the November 2020 Spending review, the UK Government announced that income tax allowances and thresholds would increase in line with the September Consumer Price Index (CPI) figure. The annual CPI increase to September 2020 was 0.5%.

Therefore, the Emergency Tax Code of 2021/2022 will increase to 1257L.

All Week 1 Month 1 Indicators will not be taken forward into 2021/2022 for any tax code.

Tax Code Uplift

All L Suffix codes will increase by +7

All M Suffix codes will increase by +8

All N Suffix codes will increase by +6

PAYE Thresholds

| Earnings Period | Threshold |

|---|---|

| Weekly | £242 |

| Monthly | £1,048 |

The current UK rate of Income Tax (excluding Scotland and Wales).

|

Tax Rate

|

Rate

|

Income after allowances from

|

Income after allowances to

|

|---|---|---|---|

|

Basic Tax Rate

|

20%

|

|

£37,700

|

|

Higher Tax Rate

|

40%

|

£37,701

|

£150,000

|

|

Additional Tax Rate

|

45%

|

£150,001+

|

|

The current Scottish rate of Income Tax (SRIT).

|

Tax Rate

|

Rate

|

Income after allowances from

|

Income after allowances to

|

|---|---|---|---|

|

Starter Basic Tax Rate

|

19%

|

£1

|

£2,097

|

|

Basic Tax Rate

|

20%

|

£2,098

|

£12,726

|

|

Intermediate Tax Rate

|

21%

|

£12,727

|

£31,092

|

|

Higher Tax Rate

|

41%

|

£31,093

|

£150,000

|

|

Additional Tax Rate

|

46%

|

£150,001 +

|

The current Welsh rate of Income Tax (WRIT).

|

Tax Rate

|

Rate

|

Income after allowances from

|

Income after allowances to

|

|---|---|---|---|

|

Basic Tax Rate

|

20%

|

|

£37,700

|

|

Higher Tax Rate

|

40%

|

£37,701

|

£150,000

|

|

Additional Tax Rate

|

45%

|

£150,001+

|

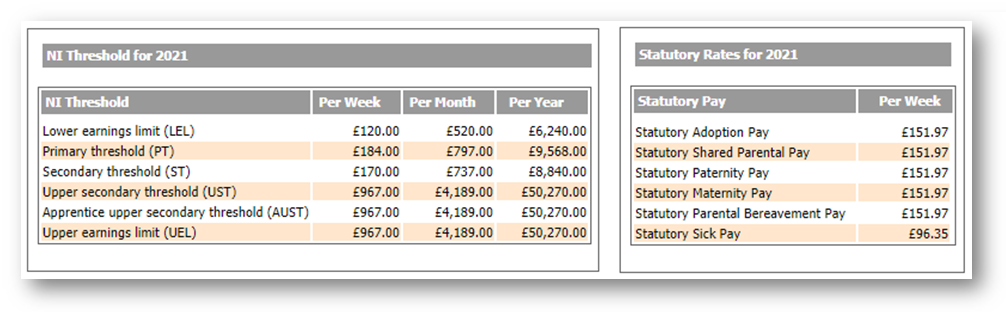

PAYE – National Insurance Threshold rates for 2021.

| NI Threshold | Weekly | Fortnightly | Lunar | Monthly | Annually |

|---|---|---|---|---|---|

| Lower Earnings Limit (LEL) | £120 | £240 | £480 | £520 | £6,240 |

| Primary Threshold (PT) | £184 | £368 | £736 | £797 | £9,568 |

| Secondary Threshold (ST) | £170 | £340 | £680 | £737 | £8,840 |

| Upper Secondary Threshold (UST) | £967 | £1,934 | £3,867 | £4,189 | £50,270 |

| Apprentice Upper Secondary Threshold (AUST) | £967 | £1,934 | £3,867 | £4,189 | £50,270 |

| Upper Earnlings Limit (UEL) | £967 | £1,934 | £3,867 | £4,189 | £50,270 |

Student Loans and Post Graduate Loans

From 6th April 2021 the breakdown between the three Student Loan Types is:

- Plan 1 has an Earnings Threshold of £19,895 per year

- Plan 2 has an Earnings Threshold of £27,295 per year

- Plan 4 has an Earnings Threshold of £25,000 per year

If the employee knows they have a student loan, but not which Plan Type, you should select Plan Type 1 as a default. HMRC will correct this with an SL1/SL2 as appropriate.

From 6th April, the Thresholds for Post Graduate loans will be:

- The Earnings Threshold will be £21,000 per year

National Minimum Wage (NMW) and National Living Wage (NLW)

From the pay period starting on or after 1st April 2021:

| Age Range | Old Rate per hour | New Rate per hour |

| Apprentices | £4.15 | £4.30 |

|

Apprentices over 19 but in 1st year of Apprenticeship |

£4.15 | £4.30 |

| Under 18 years old (but above school leaving age) | £4.55 | £4.62 |

| 18 to 20 years old | £6.45 | £6.56 |

| 21 to 22 years old | £8.20 |

£8.36 |

| 23 to 24 years old | £8.20 | £8.91 |

| 25 years old and over | £8.72 | £8.91 |

Please note: The age in which employees should be paid the National Living Wage will change from 25 years to 23 years old.

More information on the living wage and latest rates for NMW can be found at: http://www.gov.uk/national-minimum-wage-rates.

Statutory Payments - Sickness (SSP), Maternity (SMP), Paternity (SPP), Adoption (SAP), Shared Parental (ShPP), Parental Bereavement (SPBP)

Statutory Parental Payment rates will update from 4th April 2021 (the 1st Sunday of April).

Statutory Sick Payment rates will update from 6th April 2021.

| Statutory Pay | Per Week Rate |

|---|---|

| Statutory Adoption Pay | £151.97 |

| Statutory Shared Parental Pay | £151.97 |

| Statutory Paternity Pay | £151.97 |

| Statutory Maternity Pay | £151.97 |

| Statutory Parental Bereavement Pay | £151.97 |

| Statutory Sick Pay | £96.35 |

Upon rolling over into the tax year 2021/2022, all Statutory Payment Schedules will be regenerated based on the above rates where applicable.

Pension

| Qualifying Earnings Lower Threshold | Qualifying Earnings Upper Threshold | Automatic Enrolment Trigger | |||

|---|---|---|---|---|---|

| Period | Amount | Period | Amount | Period | Amount |

| Weekly | £120 | Weekly | £967 | Weekly | £192 |

| Fortnightly | £240 | Fortnightly | £1,934 | Fortnightly | £384 |

| Lunar | £480 | Lunar | £3,867 | Lunar | £768 |

| Monthly | £520 | Monthly | £4,189 | Monthly | £833 |

The Pension Diary will automatically update to 2021/2022 when your portal is rolled forward into 2021/2022

For 2021/2022 there are no planned rises in the contribution percentages, so the rates remain the same as the 2019/2020 tax year.

| Minimum Contributions for Qualifying Earnings | |

|---|---|

| Minimum Total Contributions | 8% |

| Minimum Employer Contribution | 3% |

| Required Member Contribution where Employer is minimum | 5% |

| Certification for Pensionable pay for | |||

|---|---|---|---|

| Tier 1 | Tier 2 | Tier 3 | |

| Minimum Total Contributions | 9% | 8% | 7% |

| Minimum Employer Contribution | 4% | 3% | 3% |

| Required Member Contribution where Employer is minimum | 5% | 5% | 4% |

If you require any changes to your pension scheme’s default percentage rates because you have tier certification, please send details to your payroll specialist who will ensure the changes are made from the start of the new tax year.

Tax Code Uplift

In October 2018, HMRC introduced the Finance Bill 2018-2019 which set the Personal Allowance for 2019/2020 at £12,500. And the basic rate limit at £37,500. These thresholds will remain the same for 2020/2021 and will increase in line with the Consumer Price Index (CPI) thereafter.

Therefore, the Emergency Tax Code of 2020/2021 will remain 1250L.

All Week 1 Month 1 Indicators will not be taken forward into 2020/2021 for any tax code.

Allowances

Employment Allowance - The rules around this are changing as of April 2020. There will be a separate release note outlining the system changes in relation to this.

- Employment Allowance - £4,000

- Apprenticeship Levy Allowance - £15,000

Rolling Over the Portal

Your Payroll Specialist will contact you near to the completion of your final pay run for the 2020/2021 tax year, to arrange for your portal to be rolled forward to the 2021/2022 tax year. When rolled forward, all rates and allowances will automatically update for the 2021/2022 tax year.

Comments

Please sign in to leave a comment.