What’s Changing?

Proposed Release Date: 15th March 2018

Reason for the Change

Customers Affected

Release Notes

PAYE - Tax and National Insurance:

Rates and Thresholds

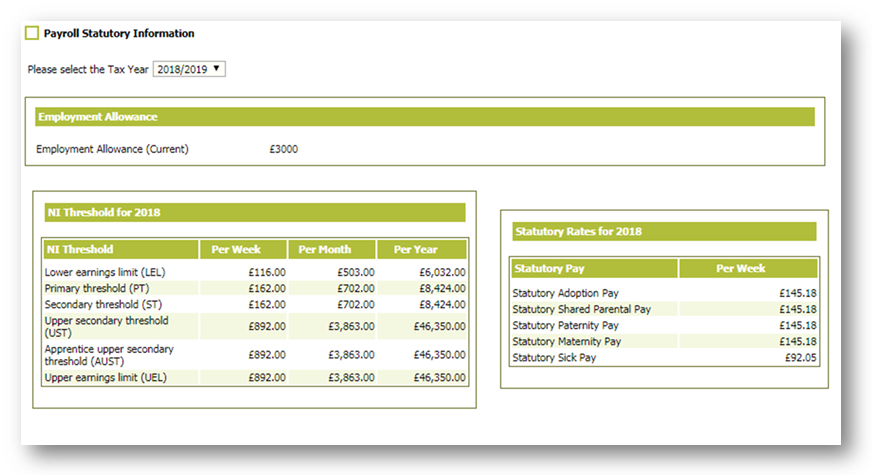

- Go to Payroll > Admin > Payroll Statutory Information Screen

The screen has been updated to provide details of Rates and Thresholds for Tax and National Insurance for 2018/19.

Fig.1 – Payroll Statutory Information

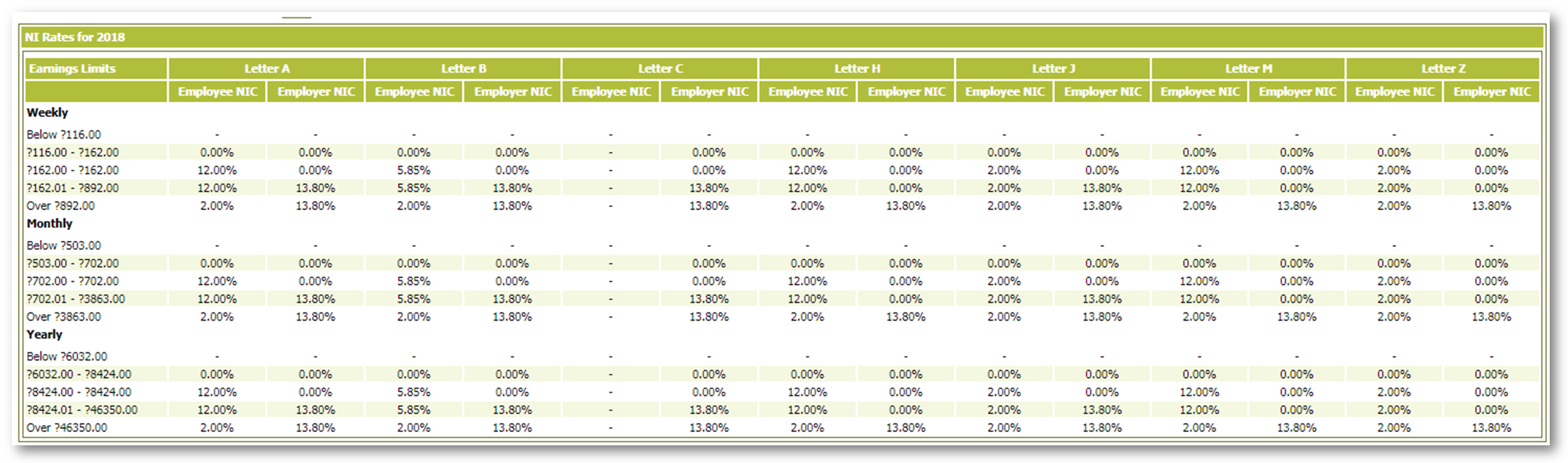

Fig.2 – NI Rates for 2018

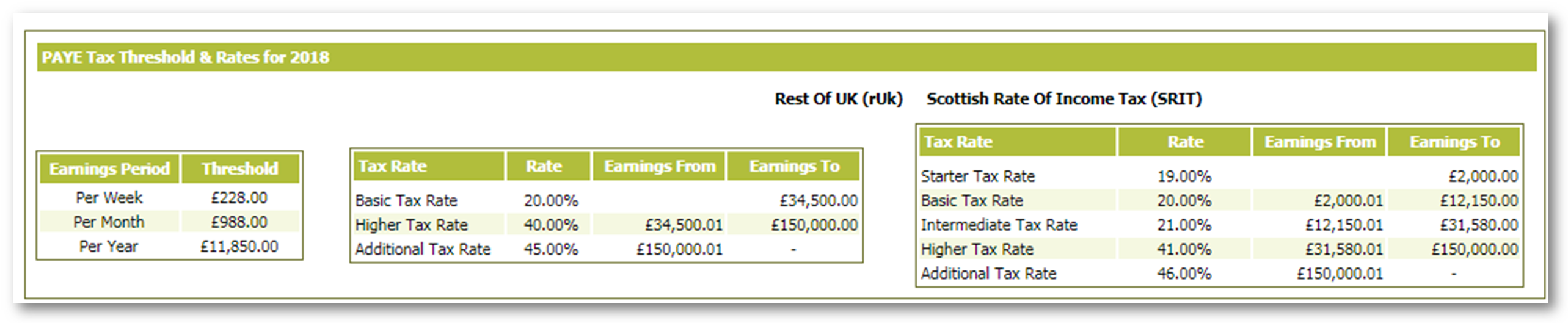

Fig.3 – PAYE Tax Thresholds & Rates for 2018

Student Loans

From 6th April 2018 the breakdown between the two Student Loan Types is:- Plan 1 with an earnings threshold of £18,330 per year

- Plan 2 with an earnings threshold of £25,000 per year

If the employee knows they have a Student Loan but not which Plan Type, you should select Plan Type 1 (see Fig.4) as a default. HMRC will correct this with an SL2\SL1 as appropriate.

Fig.4 – Employee Tax Status

Alternatively, time permitting, it may be decided to refer employees to the Student Loan Company website so they can work out which plan type they should be paying. A choice of which type to deduct can then be made as a result.

National Minimum Wage (NMW) and National Living Wage (NLW)

From 1st April 2018:

21 to 24 year olds from £7.05 to £7.38 per hour

18 to 20 year olds from £5.60 to £5.90 per hour

Under 18 £4.20 per hour

Apprentices from £3.50 to £3.70 per hour

25 and over from £7.50 to £7.83

More information on the living wage and latest rates for NMW can be found at: https://www.gov.uk/national-minimum-wage-rates

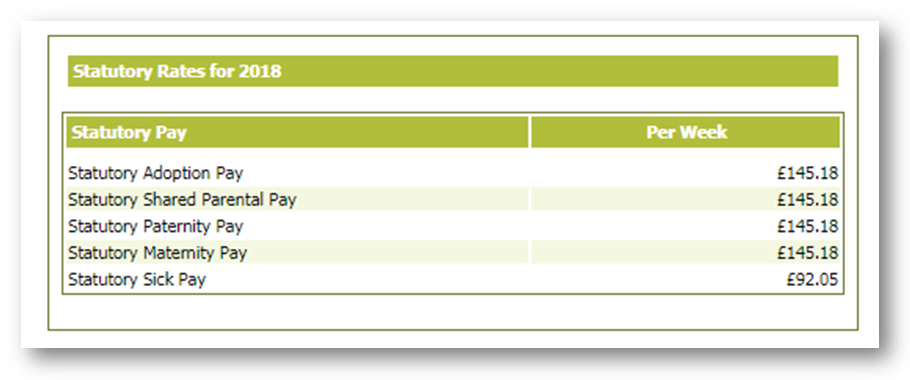

Statutory Payments – Sickness (SSP), Maternity (SMP), Paternity (SPP), Adoption (SAP), Shared Parental (ShPP)

- The rates for 2018/19 in this area can be viewed for 2018/19 in Payroll > Administration > Payroll Statutory Information

Fig.5 – Payroll Statutory Information

Upon rolling over into tax year 2018/2019 all S*P schedules will be regenerated based on the above rates where applicable.

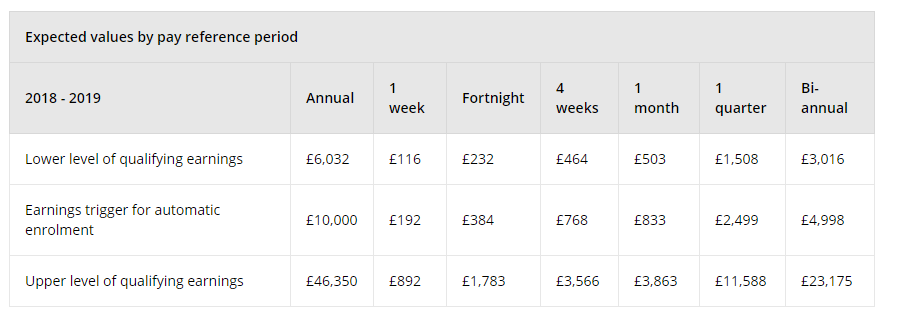

Pensions

The Department of Work and Pensions (DWP) has announced the proposed earnings thresholds for the 2018 - 2019 tax year. These values have been published in an Order (a form of secondary legislation) by the DWP and laid before Parliament and so are subject to Parliamentary approval.

Fourth received an update from The Pension Regulator (TPR) in February confirming that Parliamentary approval is still pending.

Fourth does not expect the rates and thresholds to change from the proposed rates, as shown in the table below, as these fall in line with National Insurance rates (as in previous tax years).

As soon as we receive confirmation from TPR, we will amend the system with the confirmed earnings thresholds and inform you with an additional release note that this is complete.

Fig.6 – Expected Pension Rates

- Go to Pension > Administration > Pension Scheme {select scheme} > Pension Diary

If your Pension Dairy has not already been manually updated for tax year 2018/2019, this will happen when your portal is rolled over into 2018/19.

In some circumstances you may have to edit the dates that are scheduled by the system. Therefore, when the diary is generated, it is important that you check and verify the dates, editing dates as appropriate using the edit option on each row.

Pension Phasing Legislation Changes

To cater for the minimum contribution amounts set out in legislation,all automatic enrolment schemes will have their main pension record and worker groups updated as follows:

- All Employer % contributions at pension scheme level that are below 2% but greater than 0% are updated to 2%

- All Employee % contributions at pension scheme level that are below 3% but greater than 0% are updated to 3%

- All Employer % contributions at worker group level that are below 2% but greater than 0% are updated to 2%

- All Employee % contributions at worker group level that are below 3% but greater than 0% are updated to 3%

Rolling Over the Portal:

Your Payroll Specialist will contact you near to the completion of your final pay run for the 2017/2018 tax year, to arrange for your portal to be rolled forward to the 2018/2019 tax year.

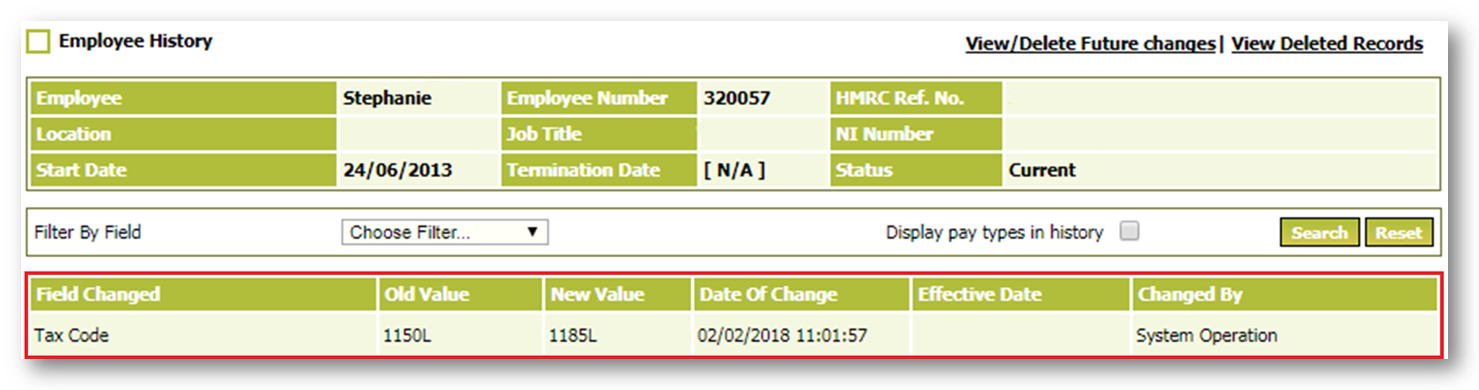

What the Rollover will do:

This section describes the changes made by the system when the Portal is rolled over into the new tax year. When viewed on the Employee History screen, these changes are indicated as a “System Operation” as per the example below:

Fig.7 – Employee History, showing a System Operation

Tax Code Uplift

From 6th April 2018 tax codes will be uplifted as per the following table:

| Tax Code Suffix | Increase |

| L | 35 |

| M | 39 |

| N | 31 |

For example:

• 11500L becomes 11850L

• 12650M becomes 13035M

• 10350N becomes 10665N

Week 1\Month1 Indicators will not be taken forward into 2018/19 on any tax code.

PAYE Rates and Thresholds:

Rates and thresholds for Tax in the UK (rUK) and Scotland (SRIT) and National Insurance will be updated for the new tax year as part of the portal roll over. As result, pay will be calculated accordingly for 2018/19 for pay dates on or after 6th April 2018.

See Payroll > Admin > Payroll Statutory Information Screen or Fig.3 for actual rates and thresholds for 2018/19.

The system will carry out a check on Payroll Preview to ensure that employees do not have any of the Contracted-Out NI categories as a current value and amend the category to the standard rate equivalent, as per the table above.

Allowances

Employment Allowance: £3,000

Apprenticeship Levy Allowance: £15,000

Comments

Please sign in to leave a comment.